Budapest: relief-rally in the stock markets, the risks remain

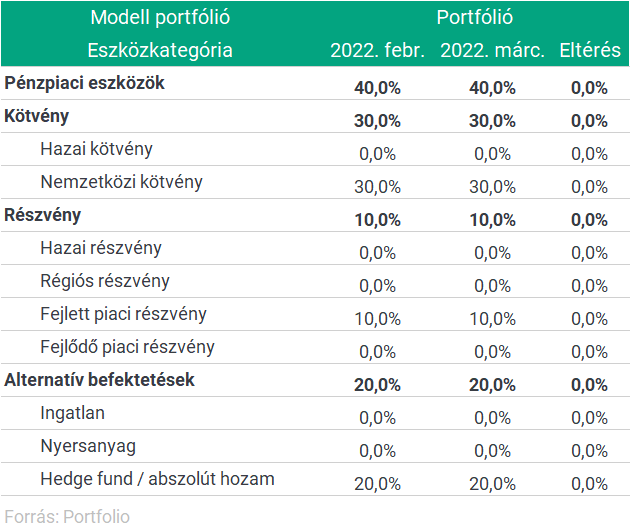

As part of our “Portfolio Referrals” series, we ask Hungarian fund managers every month how they would put together a medium-risk, medium-term, fictitious model portfolio. Below you can read the article of Budapest Fund Management:

“By the first half of March, there was also a strong fear and oversupply in stock markets by historical comparison. The second half of the month brought some relief to the war situation, so in the absence of more serious macroeconomic data, small investors were able to return to the stock markets. developed under-positioning and the alleviation of extreme pessimism played a role.

The likelihood of highly negative scenarios for the war situation has waned, and decisions taken at the NATO summit have also been cautious enough to prevent the conflict from spreading to the Russian-NATO scene. The Russian side has announced that the first phase of the military operation has been completed, the advance of the Russian army has been agreed in Kiev, but the Russian-Ukrainian peace talks in Turkey have also strengthened confidence.

The negative economic consequences of the war are not expected to be felt until next month and will last this year. The current geopolitical situation is weakening globalization processes and increasing economic polarization. Russia’s isolation from developed markets could persist, forcing the Russian leadership to build alternative-financial ties, primarily to China, India, or oil-producing countries.

Rising commodity prices – oil and gas, industrial metals and agricultural products – will further increase inflationary pressures this year, in an economic environment where central banks are already lagging behind market developments and are forced to reduce liquidity at an accelerated pace. Currently, market participants expect eight to ten interest rate hikes from the Fed, but the central bank’s balance sheet total may even be reduced (QT). Investors are only confident in the “soft-landing” scenario that the US Federal Reserve will be able to curb inflation by avoiding the recession so that the economy loses its growth dynamics but does not slip into recession. On the other hand, the flattening / inversion of the US yield curve is cautious about the outlook.

After the “relief rally” in March, a decisive change in equity exposure does not seem justified, geopolitics may persist, and central banks will continue to be forced to tighten their monetary policy amid weakening growth prospects. We maintain a low risk exposure to our portfolio while maintaining a prudent risk taker profile. “

Asset allocation is for information only.