DIANETSIS Survey: Start-ups in Greece

The new research of diANEOsis attempts to map Greek startup companies as well as the system that supports them.

Start-ups that are mainly active in the field of technology, the so-called startups, have been receiving a lot of publicity since the beginning of the last decade. On the one hand, the economic crisis led to the shrinking or collapse of many traditional products in the country and left many Greeks looking for new employment options. On the other hand, technological changes have catalyzed more and more markets internationally and presented a number of important markets. The big success stories around the world that “started in a garage” and grew rapidly, like Google, shaped not just a business environment but a broader culture, an “ecosystem.”

But how have startups evolved in Greece? The new research of diANEOsis (PDF) with the scientific supervisor of the emeritus professor at the Athens University of Economics, Ioanna-Sappho Pepelasi, and which was carried out by the consulting company Octane, attempts to map the Greek startups and the ecosystem that supports them.

startups_brochure_final-1

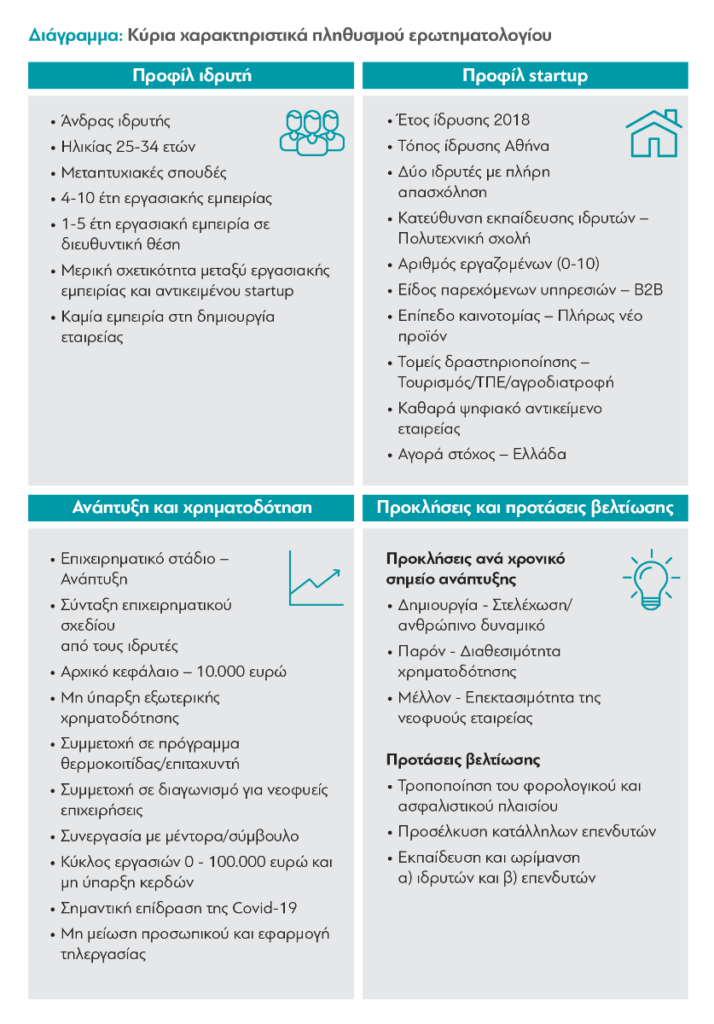

Among the startup founders who responded to the survey, the vast majority -8 out of 10- are men, an inequality observed in other European countries, which have, on average, a corresponding distribution between the sexes. In terms of age, startup founders are relatively young: 9 out of 10 are under the age of 44, while more than 50% are under the age of 34. They are also usually quite educated: 48.7% have a master’s degree and 17.2% a doctorate. Most of them declare their studies either in a Polytechnic school or in a school of business administration. 68.2% are full time at their startup.

24% have little (up to 3 years) or no previous service. 3 out of 10 founders who answered the survey are more or less more experienced, with 4 to 10 years of service, while 22.8% of the founders stated that they have significant work experience, over 15 years. Of course, although it appears from the above data that most of the respondents have some previous service, the majority (62.5%) stated that they had no previous experience in managing a start-up.

In any case, a large part of the startup founders who responded to the survey – almost 4 out of 10 – stated that their previous service concerns a job with a “neutral to non-existent” relationship with the subject of their startup. Many of them, 22.5% of the total, say they have had at least one failed business venture in the past. It is, therefore, a business that took a significant risk: many had little or no previous service, often in irrelevant subjects, while some “carried” the burden of one or more failed attempts.

Also interesting are the differences in the profile of the founders depending on whether they operate inside or outside the country. As the researchers note, “the startupper who has founded and operates the company abroad has different characteristics from the one who operates in the Region of Greece”. The startup founder abroad is more often older (35-4 years, compared to 25-34 years), has more work experience (4-10 years versus 0-3), but also more experience in management positions (1-5 ). years versus 0-1).

The “geography” of companies

Of course, in addition to the questions above themselves, as the respondents also answered questions about the companies they founded. What are the main characteristics of Greek startups?

The year in which most of them were founded compared to the other years -almost 2 in 10-, was 2018. The vast majority of startups in the sample, 93%, were founded in the period 2013-2020. More than half were founded in Athens. The next choice of the founders (15.4%) was a European city, followed by Thessaloniki (12.7%), Patras (4.5%), the USA and Heraklion (3%). The vast majority (76.4%) are very small companies with up to 10 employees. Less than 3% employ more than 50 people.

Despite their small size, startups seem to be collaborative formats. 48.3% of the companies had two founders, 19.9% three, while 13.9% more than three. Only 18% had a founder. Nearly 1 in 3 say they have drawn up their business plan with a mentor. However, the majority of the founders’ groups are also male-dominated: 62.2% are only men, while only 6.4% are women only.

In what areas are startups active? The sector in which most people are active is tourism. As is to be expected, a large percentage of these companies, almost 1 in 10, are active in information technology and communications (ICT), while a similar percentage is involved in agri-food and life and health sciences (8.6%) . It is very interesting that the order of sectors for startups abroad is a little different: ICT comes next, followed by tourism and agri-food.

Concerns and markets

But what form does the product of Greek startups have? 87.5% of companies include the use of digital technology as the original idea, while 38.6% have a clear digital idea. Fewer have a “natural” idea but have digital technology (26.6%) or, conversely, a digital idea with a partial physical presence (22.5%). Only 12.4% follow the traditional, purely natural model. In any case, it seems that the vast majority of research startups, about 7 out of 10, had to revisit the original idea, one or more times. In fact, 19.5% did it more than twice. In addition, startups are, for the most part, an extroverted activity: 63.7% say they target international customers and only 36.3% domestic. However, 1 in 3 states that their biggest problem is the lack of experience in attracting international customers.

It is also interesting that almost half of the startups in the sample started their activity with a very low capital, from zero to 10,000 euros. Only one in five (21.7%) started with a capital of more than 50,000 euros. 35.2% of these companies today declare profitable, while about half (47.9%) state that they do not profit at the present time. Regarding the biggest challenges they face for their future, the founders stand out more than any other possibility of their expansion (22.8%), followed by the staff (19.1%), the competition (16.9%), as well as and funding (15%). Among the possible changes that would improve their activity, the founders of the sample choose more than any other, the “modification of the insurance and tax framework” (79.8%).

Although the pandemic did not cause problems for startups in other companies (8 out of 10 founders say they did telework), overall the impact was rather mixed. About half of the founders in the research stressed that the Covid-19 pandemic had a negative effect on the course of their business. 28.5% of the founders believe that the pandemic had (partially or completely) a positive effect on the development of their company, while 22.8% said that it had no effect.

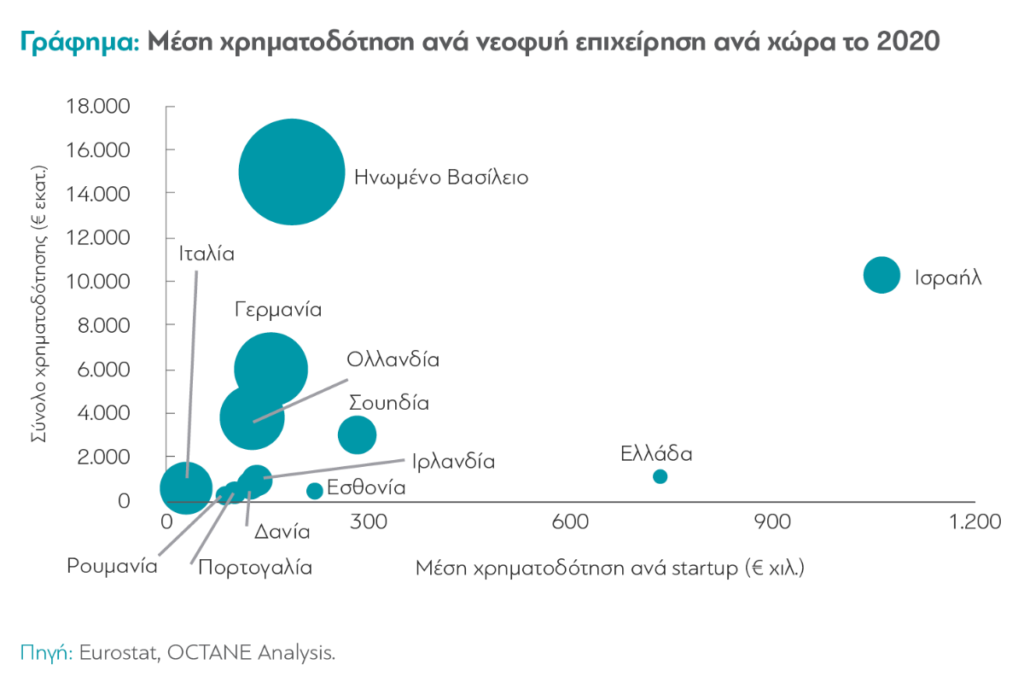

The diANEOsis survey analyzes findings, such as, for example, that startup employees are paid fairly competitive salaries, while 4 in 10 also receive company shares as a benefit. Or that in 2021 the top ten Greek startups raised four times the amount of funding raised by the top ten in 2020, an amount of about 398 million euros.

At the same time, the survey cites good practices from ten countries (nine European and Israel). Explains in detail the tax incentives it gave to investors in the UK, the policies of attracting investors to Israel, the creation of an independent university research center in Germany, the recruitment of companies to test a prototype product in the Netherlands, the incentives for Ireland’s digital public services, as well as the renewal of business centers in Italian universities. Finally, the study concludes with proposals for the further development of Greek startups, but also with a guide with many sources of information for the aspiring founders of such products.

As can be seen from the above data of diANEOsis research, startups are, like most Greek companies, very small in size. They also hire and pay well-trained employees, who exist in Greece. On the other hand, startups also gather features that are required for the evolution of the Greek production model: they are extroverted, utilized specialized knowledge and specific areas in great growth internationally. Therefore, from this point of view, their healthy development seems to be an important and wider economic opportunity for the country and for the culture of local products.