2022.09.02. Sweden is not Lithuania, Lithuanian Echo

Žygimantas Mauric

Economist

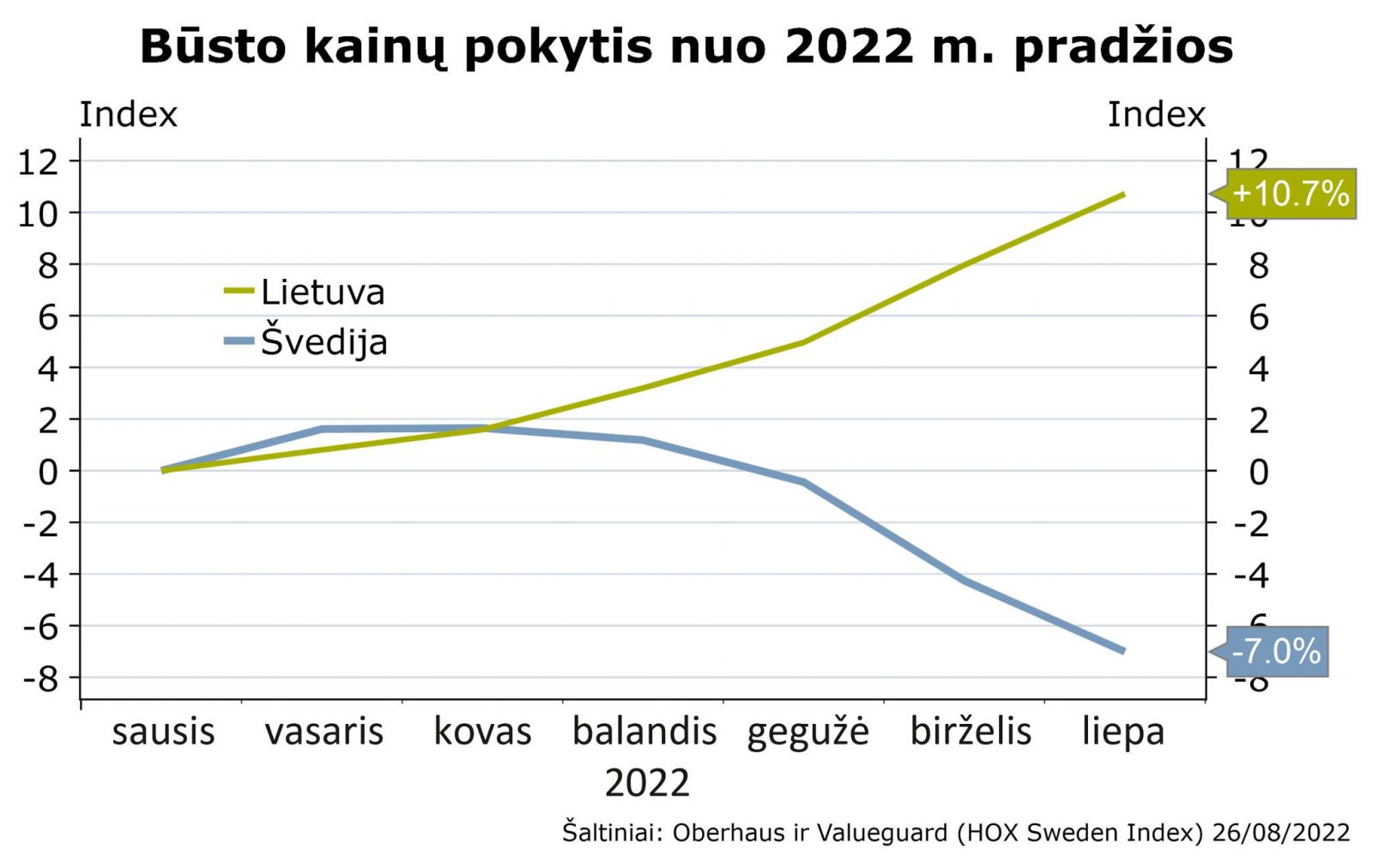

Sweden is not Lithuania, but sometimes you have to look at what is happening on the other side of the Baltic Sea. And interesting changes are taking place in the Swedish housing market: housing prices have fallen by 7% since the beginning of the year, and the number of housing transactions has decreased by double digits (apartments – 19%, and houses – 11%). The main reasons are three:

1. Extremely rapid rise in housing prices in 2020-2021 (due to the economic stimulus caused by the COVID-19 pandemic): In 2020, housing prices in Sweden grew by 7.5%, and in 2021 by another 13.7%, which is significantly faster than population income (1.6% in 2020 and 3.3% in 2021). Accordingly, housing affordability in Sweden is at an all-time low e.g. the ratio of housing prices to household income in Sweden is 35% higher than in 2007 and even 52% higher than in 1990. Let me remind you that in 1990, the bursting of the housing price bubble led to a three-year (1991-1993) economic crisis in Sweden and other Scandinavian countries.

2. Rising impact rates that make mortgages more expensive. Baseline rates in Sweden have been zero/negative since 2014, but are likely to reach 2.0% by the end of this year. The Swedish market is extremely sensitive to raising rates, as even 52% of Swedes have a home loan (the EU average is 27%, and according to this indicator, Sweden is surpassed only by the Netherlands. In Lithuania, only 14% have a home loan), and about two-thirds of the population’s home loans are with at variable related rates.

3. High inflation, which reduces the purchasing power of the population. Inflation in Sweden reaches 8.5%, and the income of the population grows by only 2-3%, so the purchasing power of the population decreases (inflation, like in other EU countries, is basically increased by the growth of energy and food prices). Accordingly, Swedish residents have less money left over to buy a home.

Lithuania has many similarities with Sweden, but there are also differences:

1. House prices in Lithuania also rose very rapidly in 2020-2021 (in 2020 they rose 5.5%, and in 2021 – 14.2%). It is true that in Lithuania, in contrast to Sweden, the incomes of residents also rose rapidly (e.g. average wages grew by 10.2% in 2020 and 10.6% in 2021), so housing affordability decreased only slightly (in the second half of 2021 and in 2022 at the beginning), which increases the resilience of the Lithuanian housing market.

2. The rising important norms also affect housing loans, but the impact of residents at macroeconomic levels should be smaller, because only 14% of Lithuania has a housing loan (in Sweden, this indicator reaches 52%), and not (about half) of housing purchase transactions in Lithuania are housing loans . However, in Lithuania, similar to Sweden, housing loans with variable rates dominate, which increases the sensitivity to rising rates.

3. Inflation in Lithuania exceeds 20% and is also higher than the growth of personal income (e.g. in the second quarter of 2022, the average wage in Lithuania grew by 13.7%, so the purchasing power of the population decreases. Accordingly, less money remains for the purchase of housing.

4. the supply of newly built housing is extremely small (especially in Vilnius), which increases the pressure for further price growth, especially since the secondary market in Lithuania is not so large, as the majority of the secondary market consists of Soviet apartment buildings, which are not attractive options for some buyers.

5. Many refugees from Belarus, Ukraine and Russia are coming to Lithuania (especially Vilnius), which increases the demand for housing (e.g. the housing market in Vilnius is red-hot, and housing rental prices have risen significantly (in Vilnius, the annual growth of apartment rental prices reaches ~ 30%), so it can support the viability of the housing market.

Conclusion: Despite the continued growth of housing prices in Lithuania in recent months, we cannot rule out the possibility of housing price correction in 2023, because, as history shows, changes in the housing market usually occur on the other side of the Atlantic Ocean* and/or the Baltic Sea. However, this time it must be large if the economy of Lithuania and the world returns to the path of sustainable growth in the second half of the next year, and international migration trends in Lithuania remain favorable.

back